This Monday: The AI-First Leader workshop

On Monday, June 22, at 10 a.m. ET, I'm running a brand new live workshop built for leaders, not practitioners. Three hours, virtual. It's not about how you personally use AI. It's about how you build an AI-first culture across an entire organization. We work through it on three levels (organizational, team, and individual) with live exercises where you audit your own business on the spot.

It's this coming Monday and seats are limited. As a newsletter subscriber, you get 40% off with the code CLAUDE40.

A few weeks ago (in issue #2) I told you that the stereotypical Harley-Davidson customer, the tattooed, bandana-wearing, beer-drinking guy you're picturing right now, accounts for barely 3.5% of Harley's revenue. The vast majority of Harley's money comes from casual, occasional buyers. They're light buyers.

This is the last issue in a series I've been writing about the Customer Demand Curve, and I want to use it to tie everything together: the curve, market share, and the most romanticized idea in all of marketing, brand loyalty.

But first, a great question I got back after the Harley issue:

"Aren't all motorcycle buyers light buyers, in the sense that a motorcycle is an infrequent purchase?"

It's a sharp question. And the answer is no.

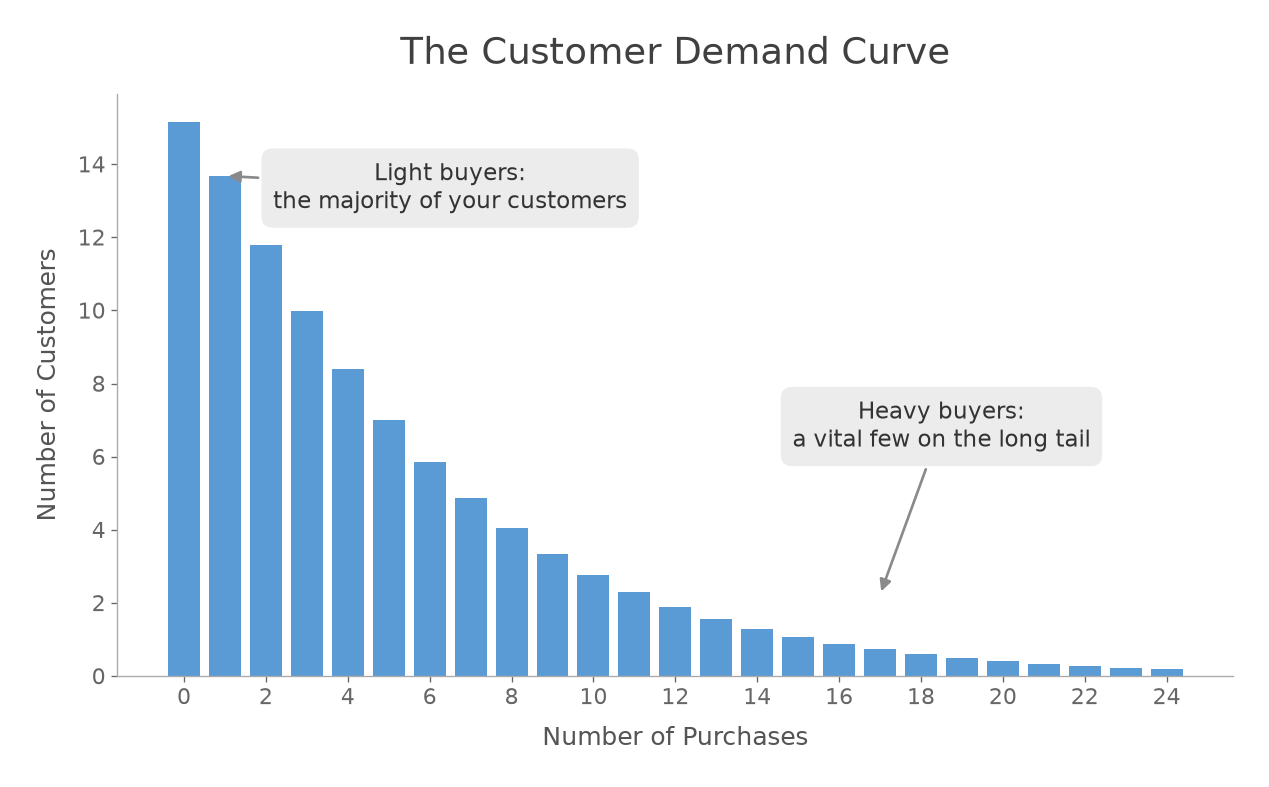

Here's the curve we've been talking about all along. Most of any brand's customers sit on the left. A vital few stretch out along the tail to the right.

In issue #4, I showed you where heavy buyers actually come from: you don't recruit them, you acquire a lot of new customers and the curve does the rest. This is true for Harley, Coca-Cola, Shopify, Disney, Lululemon, and basically every brand ever studied. There are people who collect motorcycles. A handful of them own dozens of bikes. So no, not all motorcycle buyers are light buyers.

Now here's the part I want to add, because up to this point I've been a little loose with the x-axis.

We've been plotting the number of purchases. But the thing that actually matters is revenue. And the right way to measure revenue depends entirely on your business.

For Coca-Cola, it makes sense to count cans bought in a year, because every can costs about the same and one is more or less identical to the next. Harley is different. Their bikes run from around $10,500 for an entry-level Nightster to roughly $110,000 for a top-of-the-line CVO. And almost nobody buys a motorcycle every year. So for Harley, you wouldn't measure this over twelve months. You'd measure it over ten years.

Stretch the timeline out a decade and the curve holds its shape, just in dollars. Most of the customers Harley acquires land somewhere between $10,000 and $20,000 in total revenue, which usually means they bought one Roadster and called it a day. But way out on the tail, over ten years, are customers who have spent $100,000, $200,000, and well beyond as you keep walking to the right.

iPhones make the point even better, because you'd swear they shouldn't.

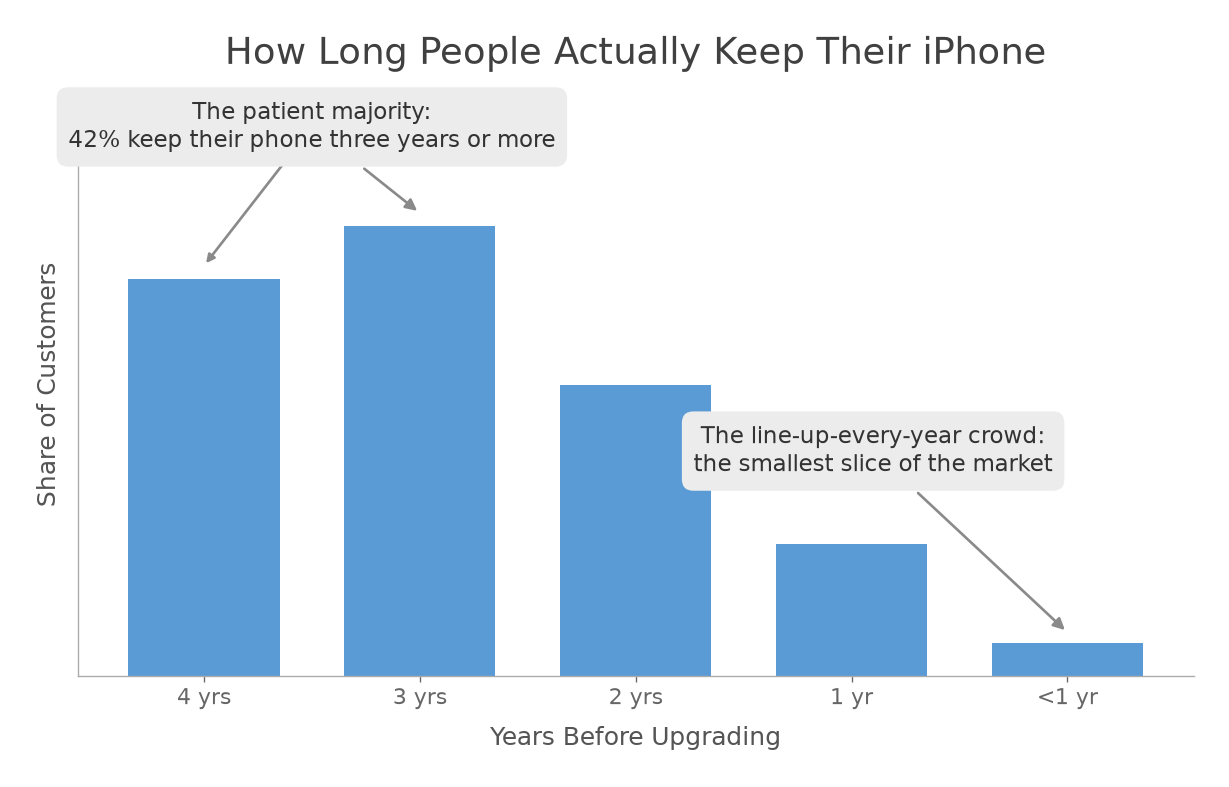

A smartphone feels like an infrequent purchase that everyone makes on roughly the same schedule. The data says otherwise. The average iPhone gets replaced about every three years. But more than 40% of people now hold onto theirs for three years or longer. (We finally convinced my mother-in-law to retire her iPhone 4 last year. She'd had it for a decade.)

On one end you have the patient majority, who keep a phone until it physically gives up. On the other end, way out on the tail, are the people who line up outside the Apple Store every September to replace a phone that isn't even a year old. Same product, same price every cycle, and the curve shows up anyway.

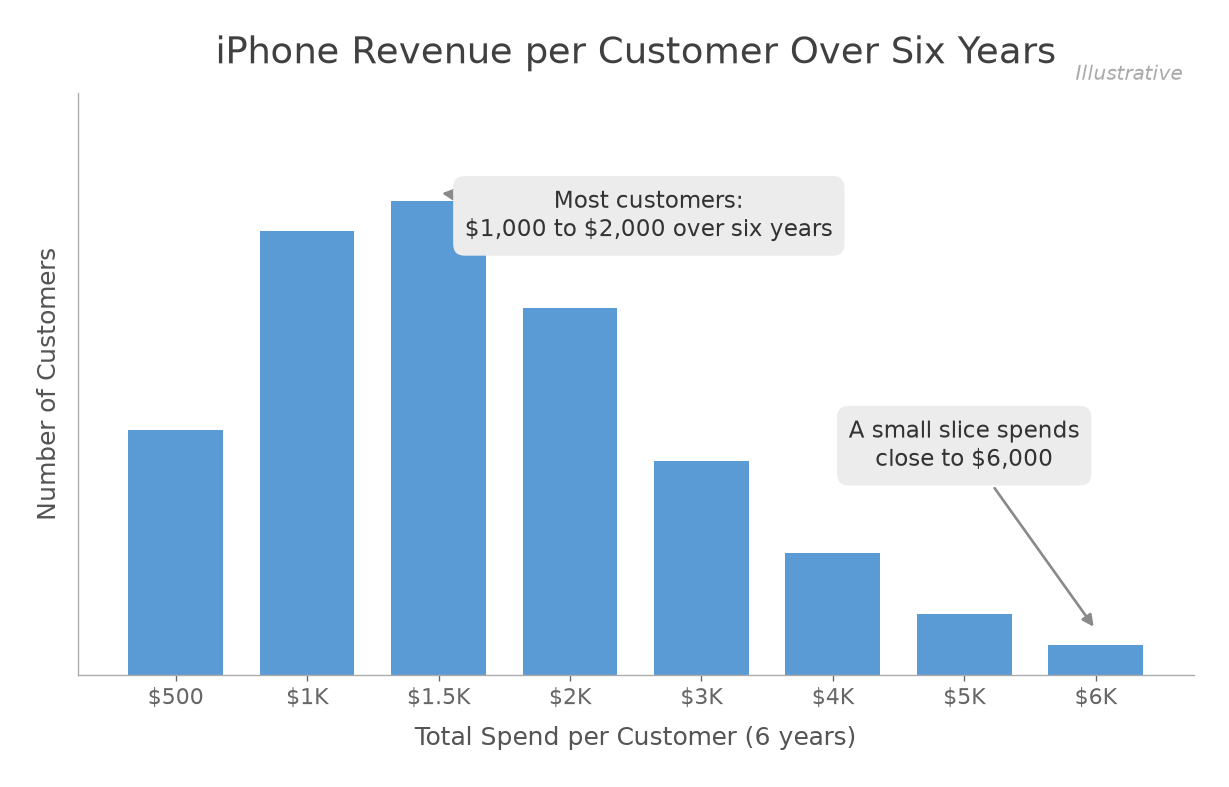

Now change the x-axis from time to dollars. Plot total revenue per customer over six years and the picture barely moves. Most people land between $1,000 and $2,000, while a small slice out on the tail spends close to $6,000. Same shape, different label.

Which brings me to lab-grown diamonds.

In the book, I tell the story of Grown Brilliance, a lab-grown diamond brand we took from zero to over $200 million in annual revenue between 2021 and 2023. When we got hired, this was the very early days of the category, and everyone we asked (including our own team) was skeptical that anyone would ever buy a lab-grown diamond. Maybe a small niche of shoppers who were lower-income, or very frugal, or deeply environmentally conscious. But scale? No chance.

We were wrong about almost all of it.

The lab-grown diamond market is now worth north of $30 billion. More than half of the engagement rings sold in the United States each year now feature a lab-grown stone (The Knot put that number at 61%). By sheer volume, this is not a niche. It is the market.

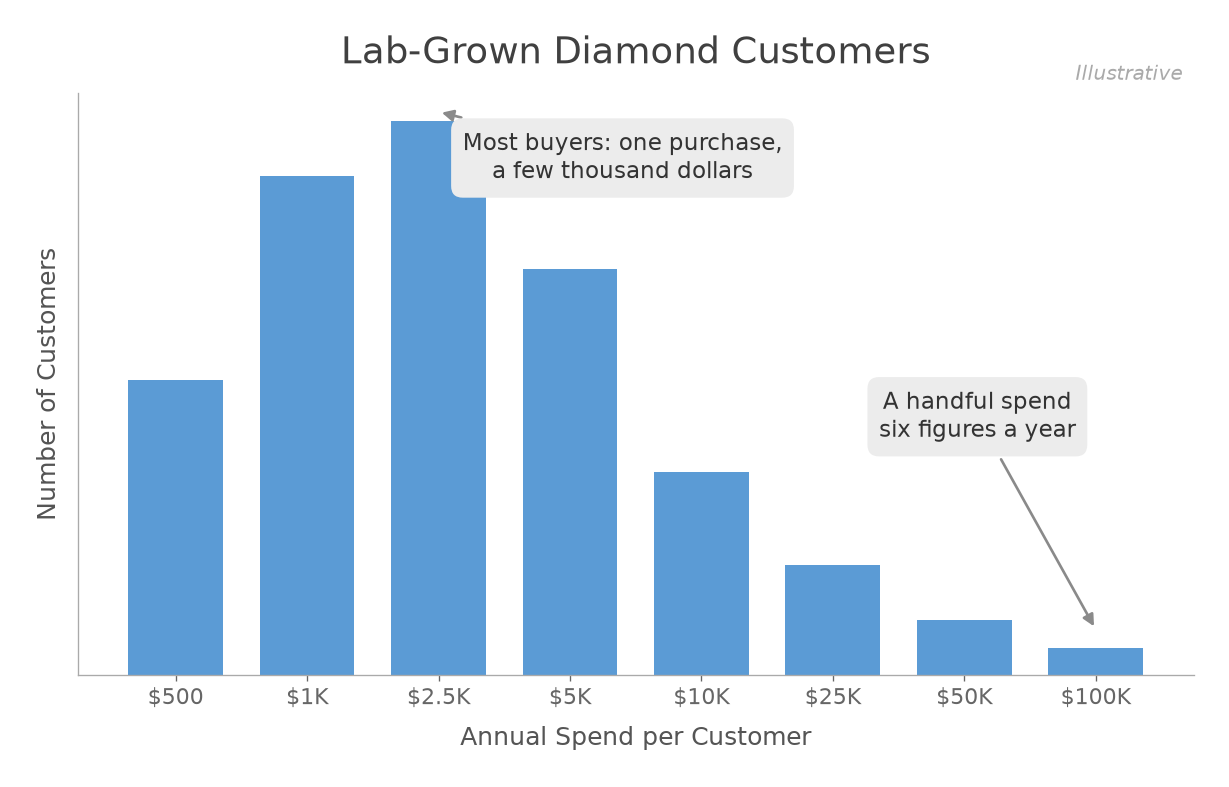

And having been on the ground floor with one of the brands that became a dominant luxury player in the space, I can tell you the single most humbling part of the whole experience was reckoning with who the customer actually was. We assumed they would be cheap or socially conscious. What we found was a mixture of everything: rich and poor, young and old, Democrat and Republican, in every corner of the country. Jewelry customers — including those shopping for an engagement ring — are mostly light buyers. Most don't buy jewelry often, and when they do, more than half the time they now choose lab-grown.

The part that genuinely shocked me was the other end of the curve.

A small set of heavy buyers came back to Grown Brilliance several times a year to spend close to or above six figures each time. Right now, on their website, you can buy a white gold diamond bracelet for $92,300! Over a hundred carats. That is a real product, on a real page, because there is a real market for it. And it is nowhere close to the most expensive thing we sold in 2023. I remember sitting in their office in Secaucus, New Jersey, in early 2023 while they showed us a custom bracelet being made for one of their ultra-high-net-worth clients. It was so heavy my colleague Nechama could barely lift it off the table.

For a long time I couldn't understand it. Why would someone with that kind of money buy lab-grown when they could obviously afford natural? The honest answer is that there is no answer. Consumers are irrational and unpredictable, which is a topic I'll spend entire future issues on. But my best guess is that almost everyone, no matter how wealthy, still recognizes value and still loves a good deal. Even with billions in the bank, your brain knows a $92,300 bracelet is a far better deal than a $200,000 one that looks the same and sits on your wrist exactly the same way.

So whether you sell a packaged good like Coca-Cola, software like Shopify, apparel like Lululemon, motorcycles like Harley, phones like Apple, or six-figure lab-grown diamond bracelets, you almost certainly have the same curve. Different axis, same shape.

Now let's talk about market share, because once you see the curve, the way most people talk about market share starts to sound wrong.

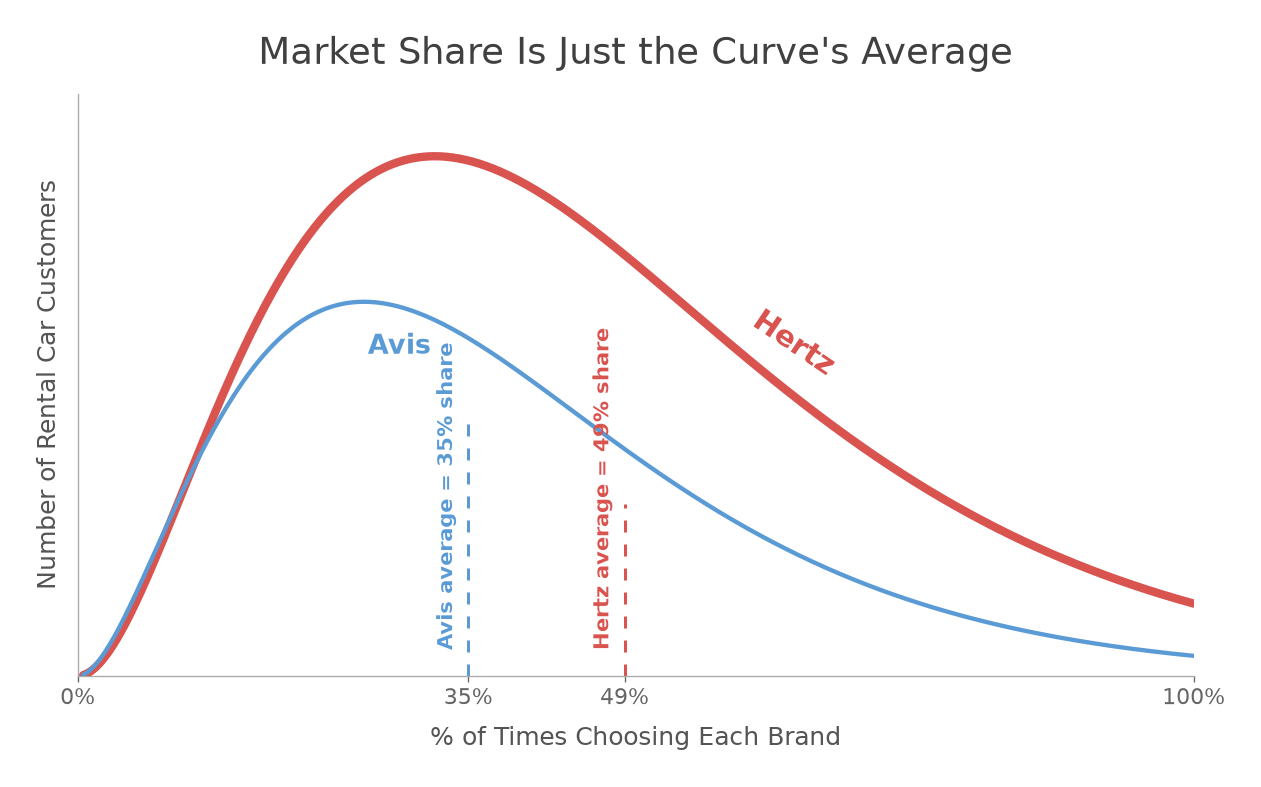

In the 1960s, Avis was the underdog in rental cars. They had about 11% of the market against Hertz's 60%, and they'd been stuck there for over a decade. Then their agency had a famous idea: stop hiding from second place. The "We Try Harder" campaign was born, and within a few years Avis had more than tripled its share to 35%, while Hertz slipped to 49%.

When you hear that Hertz has 49% of the market, your brain pictures a room of 100 people where 49 of them raise their hand and say "I'm a Hertz person." As if customers are finite, sorted, and loyal.

That's not how it works. What 49% share really means is that when someone needs a rental car, they pick Hertz 49% of the time. The same person picks Avis on a different trip. Maybe their usual airport doesn't have a Hertz counter. Maybe they booked late and Hertz was sold out, so they grabbed whatever Avis had on the lot. Even people who consider themselves loyal will, at some point, find that their brand simply isn't an option.

This is what physical availability looks like in practice, and it's why Avis spent years opening more locations. Today Avis runs roughly 1,400 rental locations across the United States. Being there when the customer is in market matters more than being loved.

But Hertz is still the more available brand. There are nearly twice as many Hertz locations in the U.S., around 2,500. That alone makes Hertz the easier default for the average traveler, and it goes a long way toward explaining why its share sits higher than Avis's.

The cleanest way I've found to picture this is to plot how often people choose each brand. Most customers sit in the middle, splitting their rentals between the two. Hertz's "49% share" is simply the average of that whole distribution, and Avis's 35% is the average of theirs. Market share isn't a headcount of loyalists. It's the mean of a curve.

So market share isn't a tug-of-war over loyalists. Brands grow by acquiring new customers, most of whom will be light buyers. When a brand gains share, the whole curve shifts and its average slides to the right. That's the entire game.

Which leaves the loyalty fallacy, the belief we cling to hardest.

We love to think our brand is top of mind, that our customers feel something for us, that there's an emotional bond holding them close. It's a comforting story. It has also been largely dismantled by Byron Sharp and the Ehrenberg-Bass Institute, through what they call the Double Jeopardy Law.

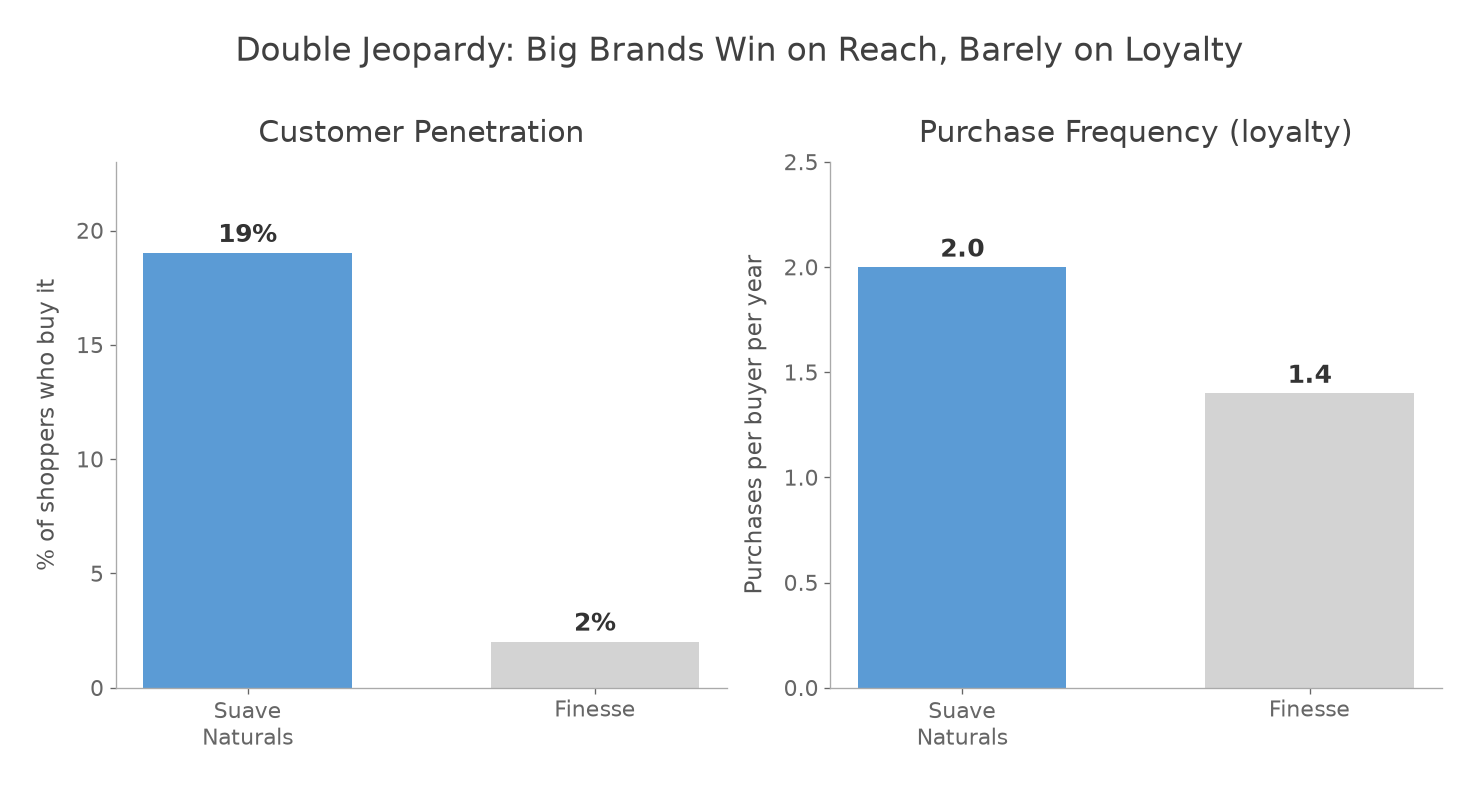

The pattern is this. Look at almost any category. Compare each brand's customer penetration (how many people buy it at all) against its average purchase frequency (a decent proxy for loyalty). What you find, almost every time, is that the biggest brands have far more customers but only slightly more loyalty.

Shampoo is a clean example. In 2005, Suave Naturals led the U.S. market: 19% of shoppers bought it, averaging two purchases a year. Finesse trailed badly, reaching just 2% of shoppers at 1.4 purchases a year.

Look at the gap. Suave reaches almost ten times as many shoppers, but buys only marginally more often. The whole difference is penetration, not devotion. And it's not because Finesse buyers shower less. It's that most Finesse buyers also buy Suave, and Pantene, and whatever bottle happens to be in front of them. They'll grab Finesse on a leisurely Target run and Suave on a rushed CVS stop because that's what's on the shelf.

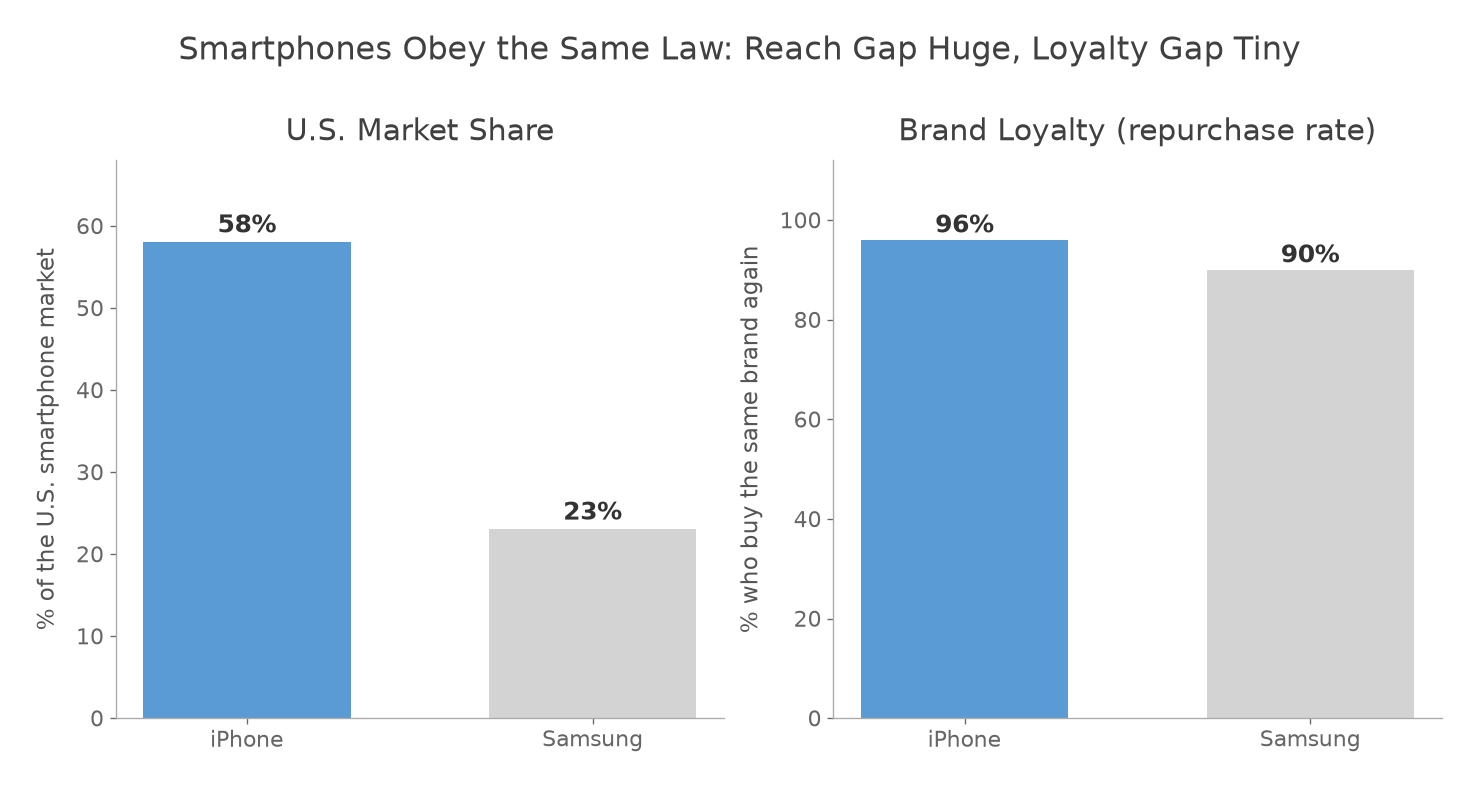

This holds across CPG, banking, insurance, cars, and yes, smartphones. In the U.S. smartphone market, the iPhone has the largest share by a mile and a little more loyalty than its rivals, but only a little. Apple keeps about 96% of its users from one phone to the next. Samsung keeps about 90%. The most dominant phone brand in the country is only a few points more loyal than its biggest competitor.

None of this should surprise us. It's exactly what happens when most of your customers are light buyers and only a handful are fanatics.

Loyalty, it turns out, is mostly a behavioral habit, not an emotional attachment. Most of us buy the same phone again because switching is annoying and we don't want to think about it. That's not love. That's convenience wearing love's clothes.

I find that more freeing than depressing. If loyalty were really about devotion, you'd be at the mercy of how people feel about you. But if it's mostly about showing up, being easy to choose, and being there when someone is ready to buy, then growth is something you can actually go build. You don't need your customers to be obsessed with you. You just need to be the easy yes when they're standing in the aisle.

That's the customer demand curve. The curve is real, share is just a bigger version of it, and loyalty is quieter than we'd like to believe.

One more thing...

Most of the corporate obsession with loyalty can be traced back to a single idea: Net Promoter Score. NPS comes from a 2003 Harvard Business Review article titled "The One Number You Need to Grow," and for two decades it has been the thing that tells companies to chase loyal, devoted customers above all else.

Two facts about where that came from.

The man who wrote it, Frederick Reichheld, was a Bain & Company consultant whose business was selling loyalty consulting. The most influential argument ever made for obsessing over loyalty came from the one person who got paid when companies suddenly decided to obsess over loyalty. Huh.

And the claim itself was never backed by real evidence. The actual examples he used in the original paper were hypothetical thought exercises. There have been no independent studies that support his original thesis.

A whole generation of loyalty programs, retention dashboards, and boardroom KPIs traces back to one article, by one consultant, who never actually proved the thing he was selling.

So once again, I'll remind you to focus on customer acquisition, knowing that most new customers will be light buyers, and a small portion will become habitually loyal heavy buyers. That is the recipe for growth.

This series pulled from several chapters of Never Always, Never Never. If someone on your team is still chasing loyalty as if it's an emotion they can manufacture, forward them this one.

Get the book on Amazon | Leave a review

Last call: The AI-First Leader workshop is this Monday

On Monday, June 22, at 10 a.m. ET, I'm running my new live workshop on building an AI-first culture across your entire organization. Three hours, virtual, built for leaders, not practitioners. Seats are limited and it's only a few days away.

As a newsletter subscriber, you get 40% off with the code CLAUDE40.